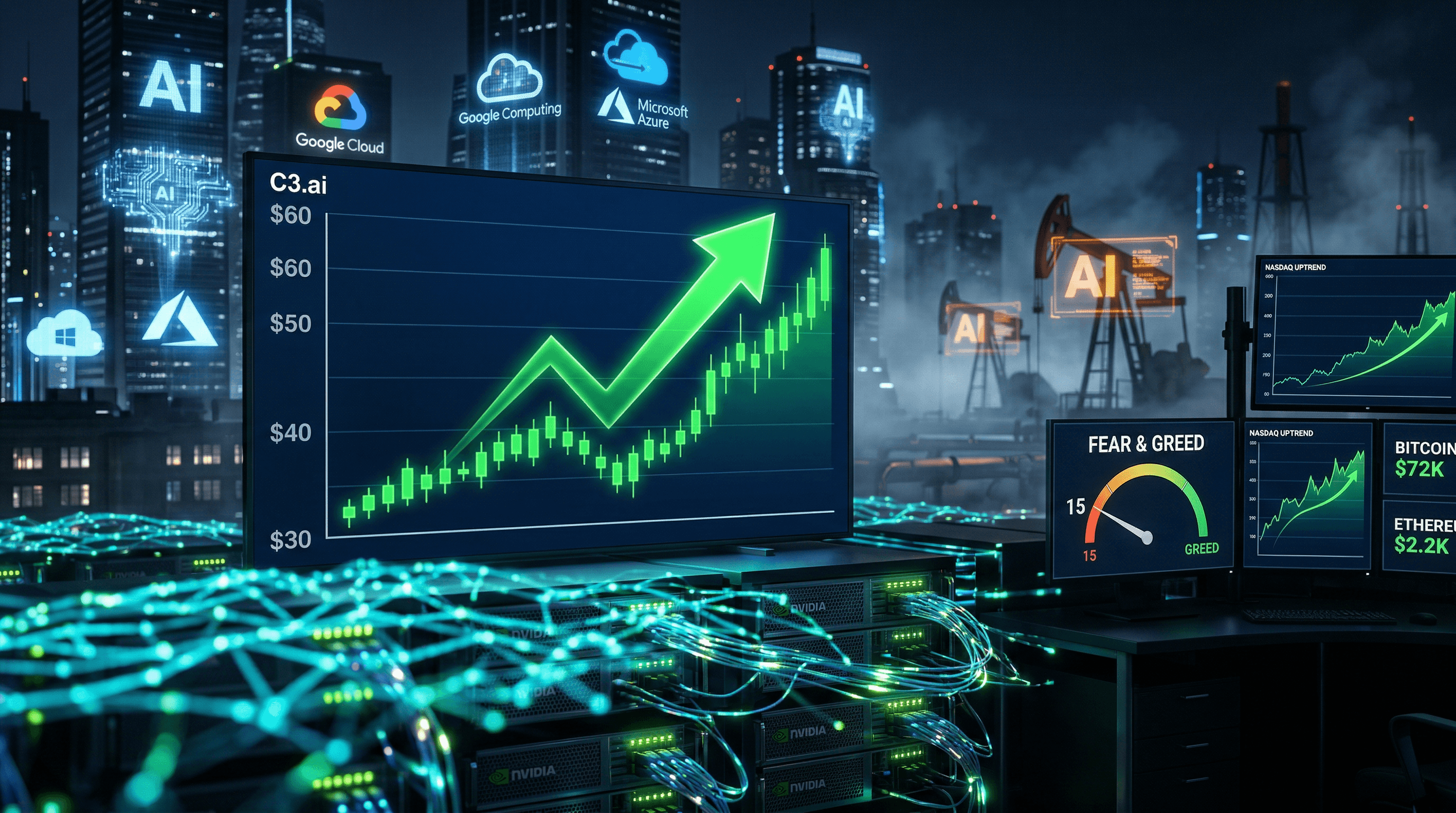

Motley Fool predicts C3.ai (NYSE: AI) shares will double to $60 by December 31, 2026. Shares closed at $30.25 on April 11, 2026. Surging enterprise AI demand fuels this outlook.

C3.ai Enterprise AI Momentum

C3.ai reported 28% year-over-year revenue growth to $85 million in fiscal Q3 2026 earnings on April 9, 2026. It beat estimates by 5%, per Bloomberg. Enterprise clients hit 120, up 15% quarter-over-quarter.

Google Cloud and Baker Hughes partnerships embed AI in oil, gas, and manufacturing. Executives project 30% revenue growth for fiscal 2027. Generative AI suite adoption rose 40% since January 2026, per SEC filings.

The platform processes 1 petabyte daily and runs 500 million inferences. Fortune 500 firms use it for supply chain and predictive maintenance. Average revenue per customer: $2.5 million annually. New deals include Shell for energy optimization and Lockheed Martin for defense simulations.

Generative AI apps now serve 50+ clients, with usage hours up 60% year-over-year. C3.ai expanded AI Foundry for no-code enterprise model building.

Market Sentiment Signals Tech Recovery

CNN Fear & Greed Index reached 15—extreme fear—on April 11, 2026. Nasdaq Composite climbed 1.2% that day. Bitcoin hit $72,963 (up 1.1%), Ethereum $2,246 (up 1.3%), showing risk appetite return.

Yale School of Management data shows stocks often double post-fear bottoms. AI stocks like C3.ai lead rebounds. In 2022, C3.ai surged 150% from lows in 18 months.

Tech rotation favors AI software over hardware as inflation cools. Enterprise AI venture funding reached $12 billion in Q1 2026, per PitchBook.

Financial Projections and Catalysts

FactSet consensus forecasts $400 million revenue for fiscal 2026, up 32% year-over-year, with EPS of $0.85. Doubling to $60 implies $25 billion market cap.

Forward P/E at 45 trails Nvidia's 60, per Yahoo Finance. Cash reserves top $750 million; debt under 10% of equity.

Catalysts: Q4 earnings June 5, 2026; new defense contracts; $5 billion U.S. government AI spend. Gartner projects AI market at $300 billion by end-2026, enterprise segment up 35% annually.

Manufacturing supplies 25% revenue, defense 20%. Analysts see contract backlog at $1.2 billion by year-end.

Valuation Comparison

C3.ai's EV/Sales ratio: 8, below industry 12, per Seeking Alpha. Palantir: 15; Snowflake: 20. Q3 gross margins hit 62%.

Rule of 40 score (growth + margins): 90, topping peers. Free cash flow turned positive at $20 million quarterly.

Risks to AI Stock Prediction

Snowflake and Databricks cut C3.ai's database share 5% last quarter, per IDC. Operating margins dropped to 15% from pricing pressure.

Fed funds rate: 4.5%; recession odds 25%, per CME FedWatch. Shares fell 20% in March 2026 on delayed deals.

Headwinds: slowing hyperscaler AI capex; top 10 clients 40% of revenue.

Investment Outlook

12 of 15 analysts rate C3.ai a buy, average target $55. Fear & Greed at 15 marked bottoms 80% of time since 2018, per CNN.

Watch April 15, 2026, Fed minutes for rate cuts. This AI stock prediction targets 100% upside by 2026 amid accelerating enterprise AI adoption.